Hello all,

The time flies very fast, and like every month, we have again a bunch of interesting improvements we would like to present to all of you.

Firstly, let’s recapitulate Quantpedia Premium development. Ten new Quantpedia Premium strategies have been added to our database, and twelve new related research papers have been included in existing Premium strategies during the last month. Additionally, we have produced 11 new backtests written in QuantConnect code. Our database currently contains over 430 strategies with out-of-sample backtests/codes.

And now, let us present the two new reports for our Quantpedia Pro subscription offering.

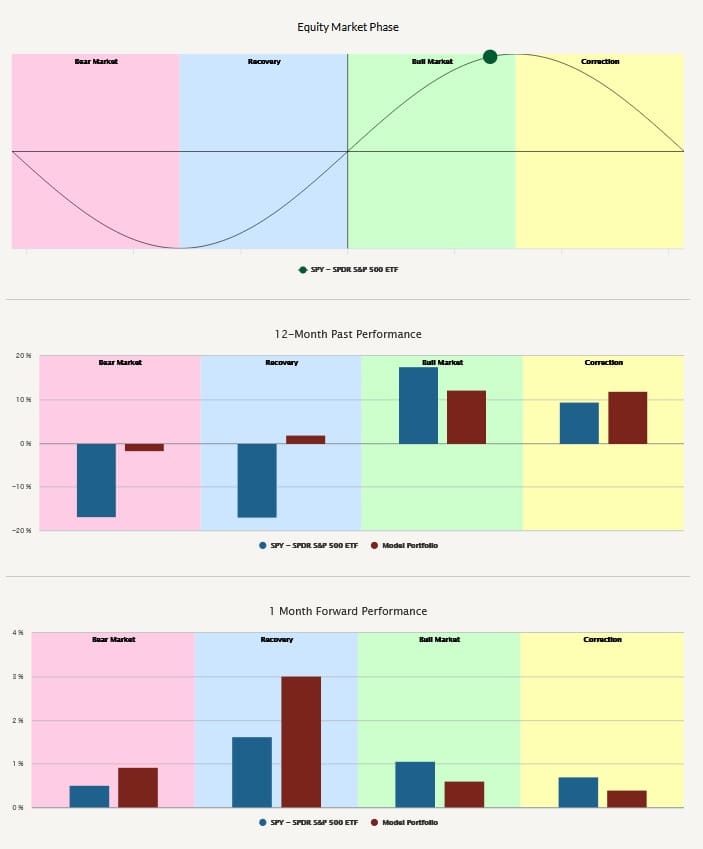

The first one, the Market Phase Analysis report, is once again inspired by the idea described in the “Momentum Turing Points” research paper written by Garg, Goulding, Harvey and Mazzoleni. Once again, we decompose the equity market (we use the SPY ETF as a proxy for the dominant equity market) into the four phases (Bull Market, Correction, Bear Market, Recovery). Afterwards, the report offers the possibility to investigate past 12-months performance and future 20-day correlation of benchmark SPY ETF and model portfolio in each of those four phases. Additionally, user can also review the future average 1-, 3-, 6- and 12-months performances (and their 20th to 80th percentile interval) of SPY and model portfolio in each market phase.

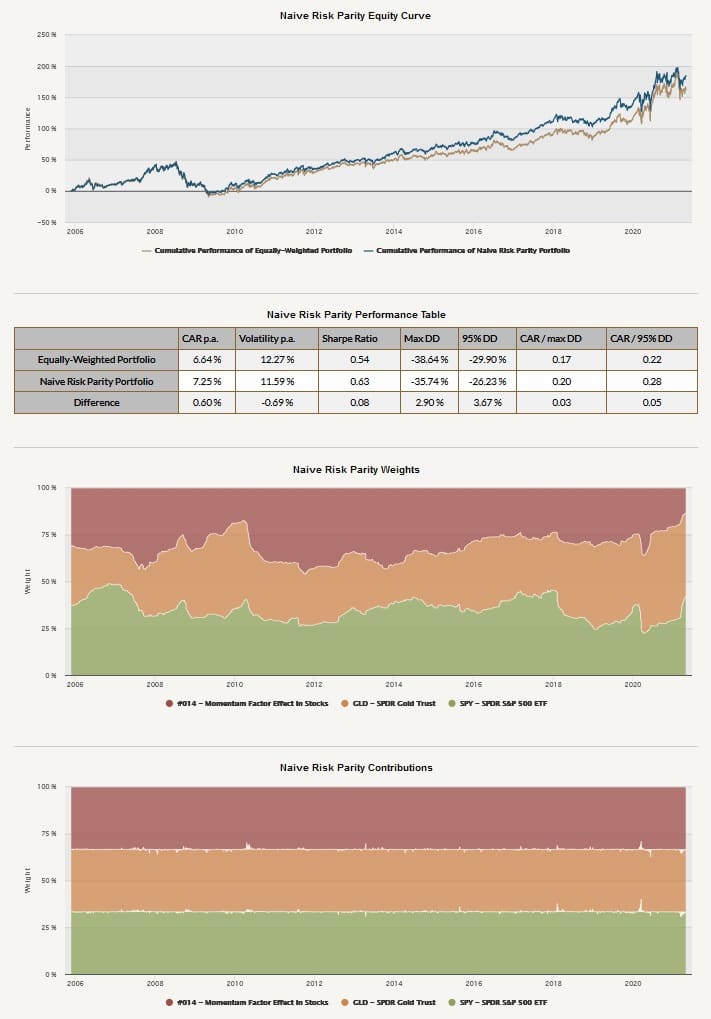

The second new Quantpedia Pro report is related to the Risk Parity portfolio allocation strategy. It calculates the model portfolio’s weights based on the inverse volatility methodology and compares Risk Parity’s performance and risk contributions to an equally-weighted benchmark portfolio. In May, we will extend this report to cover also Equal Risk Contribution and Maximum Diversification methods. A short research article that will explain all Risk Parity methodologies in more detail will be published in a few days.

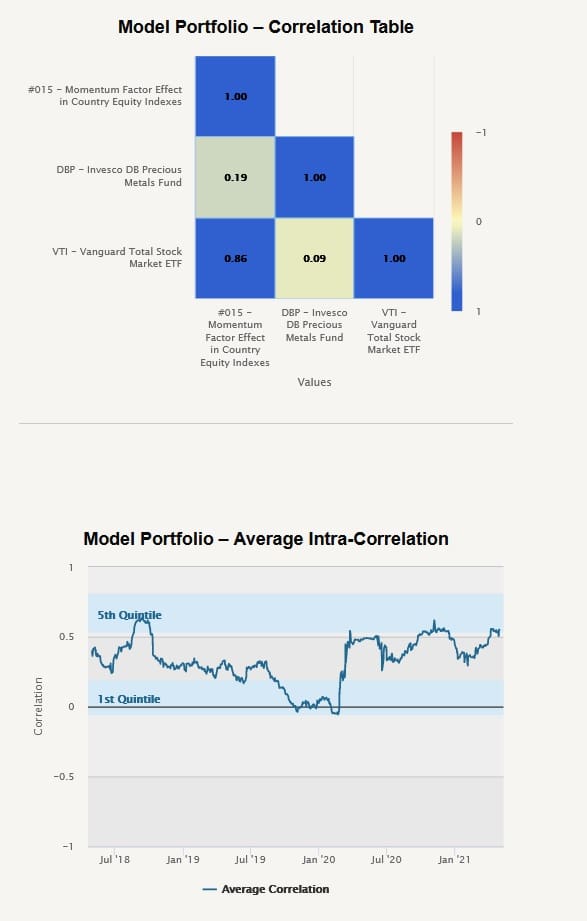

Additionally, we have added a correlation matrix and a new chart that displays average portfolio intra-correlations over time (average correlations between model portfolio’s individual constituents) into the Correlation Analysis report.

And finally, four new blog posts that you may find interesting have been published on our Quantpedia blog in the previous month:

Hunt for Yield

Autores: Hao Jiang, Lily Li and Lu Zheng & Alexandru Barbu, Christoph Fricke and Emanuel Moench & Matthijs Korevaar

Titles: Beware of Chasing Yield: Bond Fund Yield, Flows and Performance & Procyclical Asset Management and Bond Risk Premia & Reaching for Yield: How Investors Amplify Housing Booms and Busts

Market Sentiment and an Overnight Anomaly

Author: Daniela Hanicova

Título: Market Sentiment and an Overnight Anomaly

Crowding in Commodity Factor Strategies

Author: Wenjin Kang, K. Geert Rouwenhorst and Ke Tang

Título: Crowding and Factor Returns

An Analysis of Volatility Clustering of Equity Factor Strategies

Author: Dominik Cisar

Título: An Analysis of Volatility Clustering of Equity Factor Strategies

Stay safe …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube