Hello all,

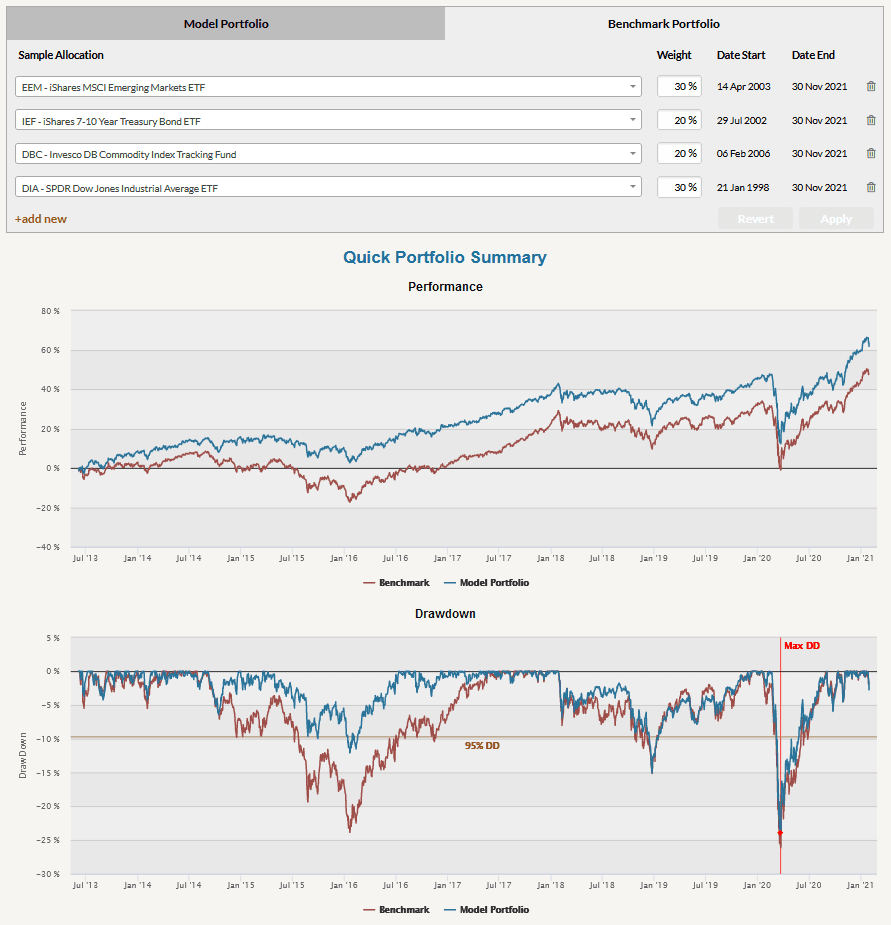

As usual, let me use this space to recapitulate what’s new in November’s update of Quantpedia’s services. The most interesting addition has been built for Quantpedia Pro‘s Portfolio Manager, which now allows you to construct a Benchmark Portfolio to complement your Model Portfolio allocation.

This feature speeds up the research process as you can now set up one default multi-strategy multi-asset portfolio as your Benchmark and then test various small changes and variations of your allocation in your Model Portfolio. Information about Benchmark allocation is directly used in a lot of Quantpedia Pro reports, such as Basic Overview, Crisis, Trend/Reversal, y Market Phases Analysis or different asset allocation reports like Volatility Targeting o Portfolio Risk Parity.

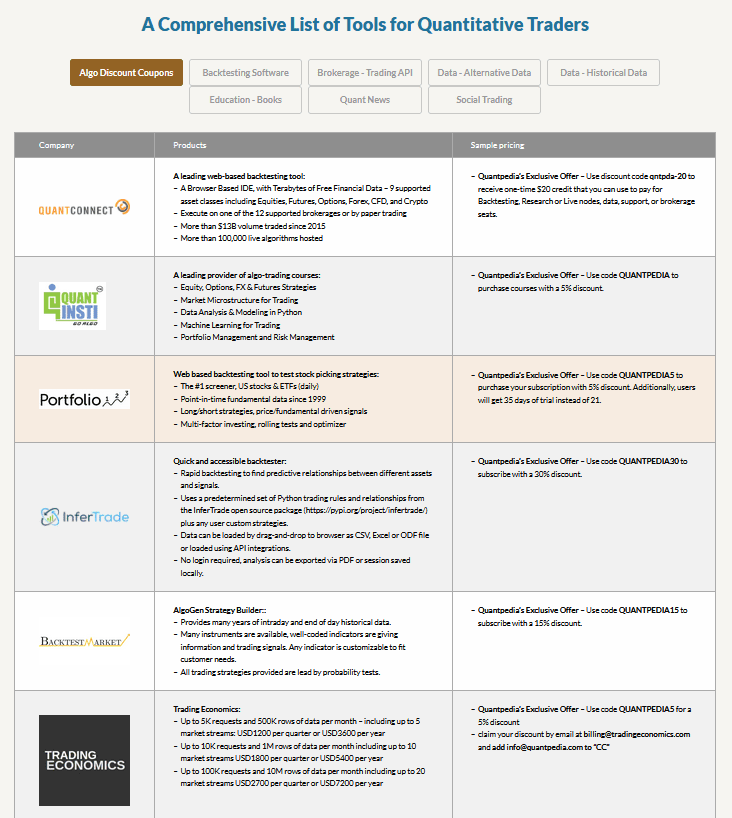

The second interesting addition is a part of our free content in the “Recursos” sub-page. We would like to let you know about a new table in the Links section. The new “Descuentos en Algo Trading” table compiles discounted offers that we were able to negotiate exclusively for our readers with some of our partners that service the algo&quant trading community.

Let’s also quickly recapitulate Quantpedia Premium development:

- 10 new Quantpedia Premium strategies have been added to our database

- 10 new related research papers have been included in existing Premium strategies during the last month

- 10 new backtests were written in QuantConnect code. Our database now contains over 500 strategies with out-of-sample backtests/codes.

Additionally, 7 new articles were published on the Quantpedia blog in the previous month, 5x analysis of academic research papers and 2x Quantpedia studies:

- Community Alpha of QuantConnect – Part 4: Composite Social Trading Multi-Factor Strategy

- How to Combine Different Momentum Strategies

Analysis of research papers:

Out-of-Sample Dataset Before the “Sample”: Pervasive Anomalies Before 1926

Autores: Guido Baltussen, Bart P. Van Vliet and Pim Van Vliet

Título: The Cross-Section of Stock Returns before 1926 (And Beyond)

The Quant Cycle – The Time Variation in Factor Returns

Author: David Blitz

Título: The Quant Cycle

How News Move Markets?

Autores: Mark Kerssenfischer and Maik Schmeling

Título: What Moves Markets?

Bitcoin Returns and Volatility Predicted by Bitcoin Exchange Reserves

Autores: Lai T. Hoang, Dirk G. Baur

Título: Effects of Bitcoin Exchange Reserves on Bitcoin Returns and Volatility

What Drives Volatility of Bitcoin?

Autores: Štefan Lyócsa, Peter Molnár, Tomáš Plíhal and Mária Širaňová

Título: Impact of macroeconomic news, regulation and hacking exchange markets on the volatility of Bitcoin

Happy trading …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube