Hello all,

Being a trader or portfolio manager is a stressful job. Sometimes, you outperform your peers, and other times you underperform. What’s important is to understand the drivers behind those swings in the performance.

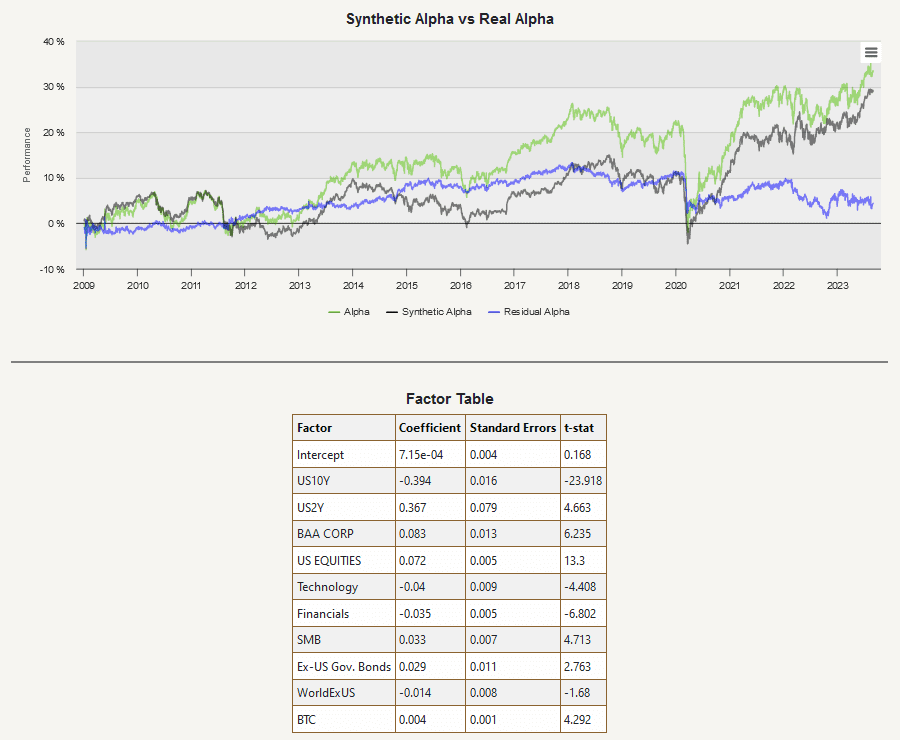

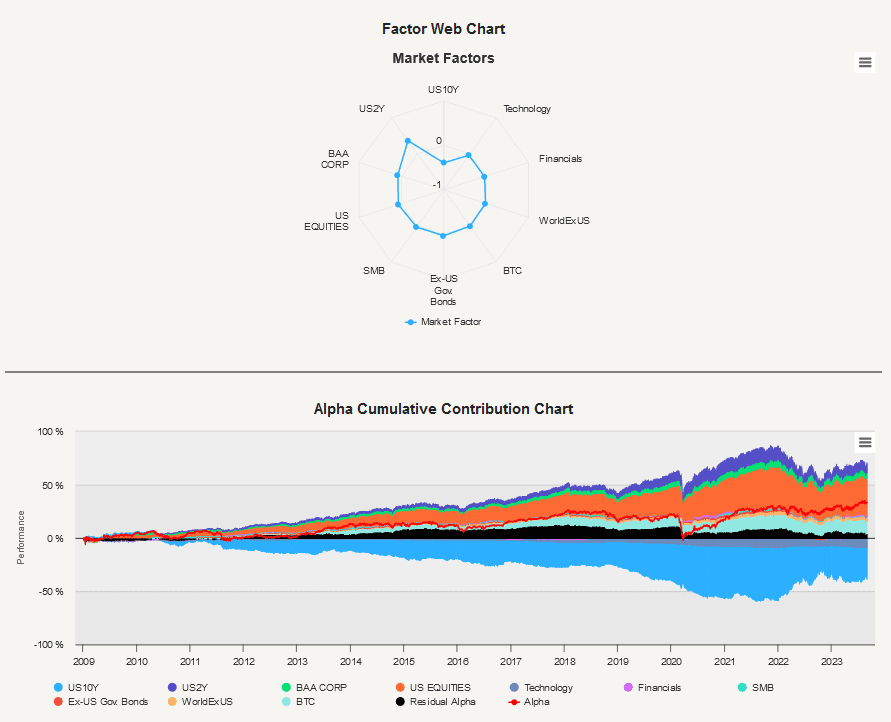

We at Quantpedia want to help with that; therefore, we have prepared a new Alpha Analysis report for our Quantpedia Pro clients. You can compare the performance of your model portfolio (built from any combination of our strategies, ETFs, or your uploaded equity curves) to your desired benchmark and investigate the differences. The new functionality provides comprehensive factor analysis, builds “synthetic alpha” that’s explainable by systematic factors, and enables users to identify the primary drivers of underperformance or outperformance of your model portfolio or trading strategy.

You can dig deeper into the intricacies of your alpha, figure out what was (or wasn’t) working and analyze the contribution of individual factors to your total out-performance. We believe that this new functionality will help you to make more informed decisions, improve your investment strategies, and ultimately achieve better results.

Let’s also quickly recapitulate Quantpedia Premium development:

- 13 new Quantpedia Premium strategies have been added to our database

- 11 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently now contains nearly 730 strategies with out-of-sample backtests/codes.

Additionally, 4 new articles were published on the Quantpedia blog in the previous month:

What Can We Extract From the Financial Influencers’ Advice?

Authors: Ali Kakhbod, Seyed Mohammad Kazempour, Dmitry Livdan, and Norman Schuerhoff

Title: Finfluencers

Military Expenditures and Performance of the Stock Markets

Autores: Cyril Dujava, Radovan Vojtko

Título: Military Expenditures and Performance of the Stock Markets

Less is More? Reducing Biases and Overfitting in Machine Learning Return Predictions

Autores: Clint Howard

Título: Less is More? Reducing Biases and Overfitting in Machine Learning Return Predictions

Decreasing Returns of Machine Learning Strategies

Autores: Nusret Cakici and Christian Fieberg and Daniel Metko and Adam Zaremba

Título: Predicting Returns with Machine Learning Across Horizons, Firms Size, and Time

Yours …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube