Related to multiple strategies, mainly to Carry, Volatility Selling and Trend-Following strategies …

Autores: Sepp

Título: Diversifying Cyclicality Risk of Quantitative Investment Strategies (Presentation Slides)

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2980708

Abstracto:

What is the most significant contributing factor to the performance of a quantitative fund: its signal generators or its risk allocators? Can we still succeed if we have good signal generators but poor risk management?

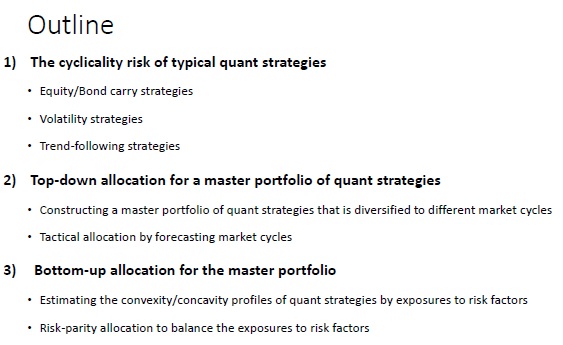

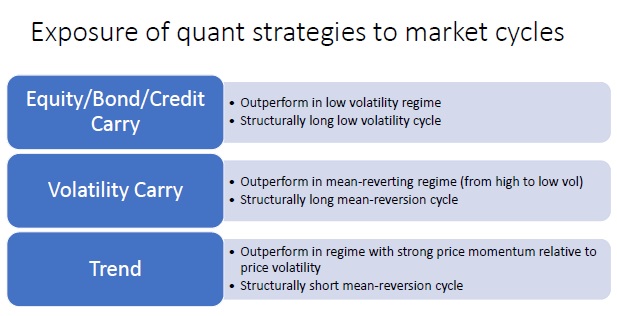

We consider the risk of the skewness and the cyclicality of the key quantitative strategies:

1. Carry strategies

2. Volatility strategies

3. Trend-following strategies

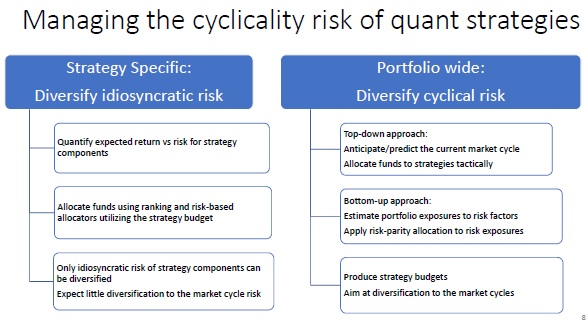

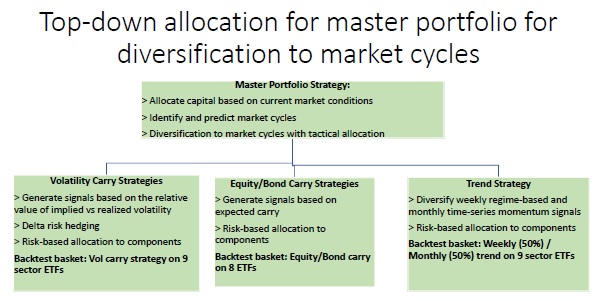

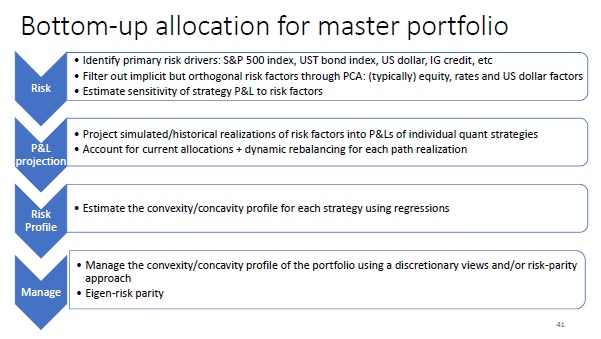

We then present the two approaches for diversification of the cyclicality risk for a master portfolio of these strategies using:

1. Top-down allocation

2. Bottom-up allocation

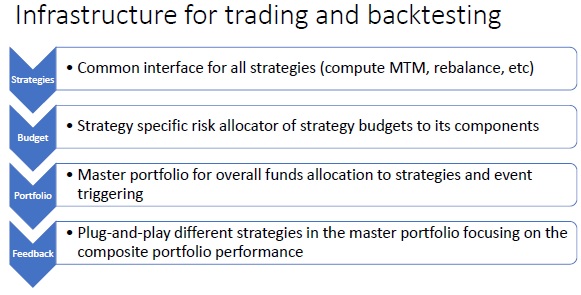

We illustrate a few examples using back-tested data using systematic quantitative strategies with risk-based allocators.

Fragmentos destacados del artículo de investigación académica:

"

"

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube