All of us at Quantpedia are history freaks, thefore we absolutely LOVE papers like this:

Autores: Schmelzing

Título: Eight Centuries of the Risk-Free Rate: Bond Market Reversals from the Venetians to the ‘VaR Shock’

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3062498

Abstracto:

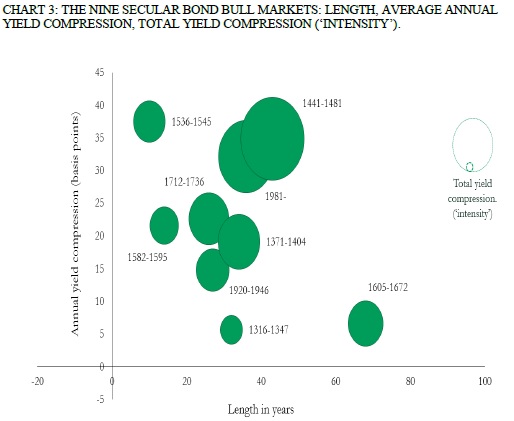

This paper presents a new dataset for the annual risk-free rate in both nominal and real terms going back to the 13th century. On this basis, we establish for the first time a long-term comparative investigation of ‘bond bull markets’. It is shown that the global risk-free rate in July 2016 reached its lowest nominal level ever recorded. The current bond bull market in US Treasuries which originated in 1981 is currently the third longest on record, and the second most intense.

The second part of this paper presents three case studies for the 20th century, to typify modern forms of bond market reversals. It is found that fundamental, inflation-led bond market reversals have inflicted the longest and most intense losses upon investors, as exemplified by the 1960s market in US Treasuries. However, central bank (mis-) communication has played a key role in the 1994 ‘Bond massacre’. The 2003 Japanese ‘VaR shock’ demonstrates how curve steepening dynamics can create positive externalities for the banking system in periods of monetary policy and financial uncertainty.

The paper finally argues that the inflation dynamics underlying the 1965–70 bond market sell-off in US Treasuries could hold particular relevance for the current market environment.

Fragmentos destacados del artículo de investigación académica:

"The most interesting charts:

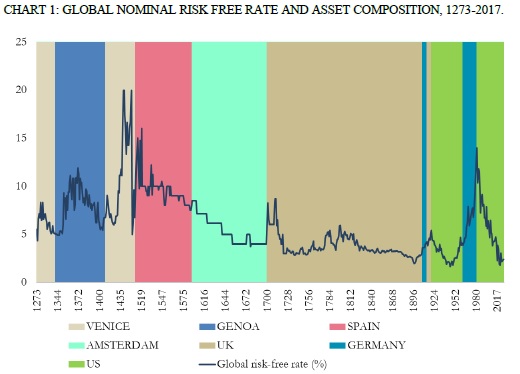

Nominal risk-free rate:

Bond bull markets comparison:

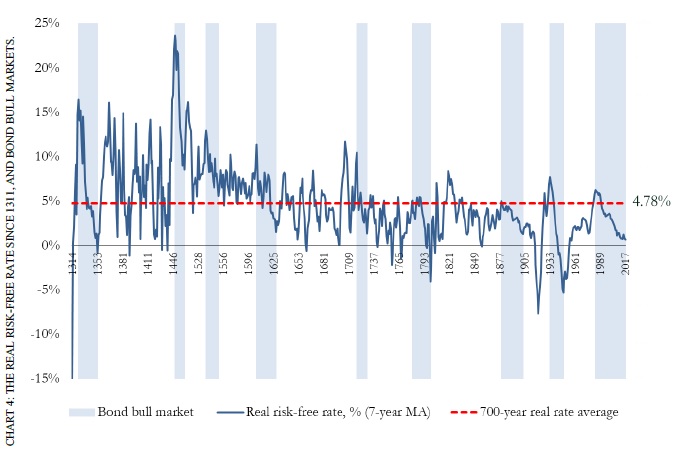

Real risk-free rate:

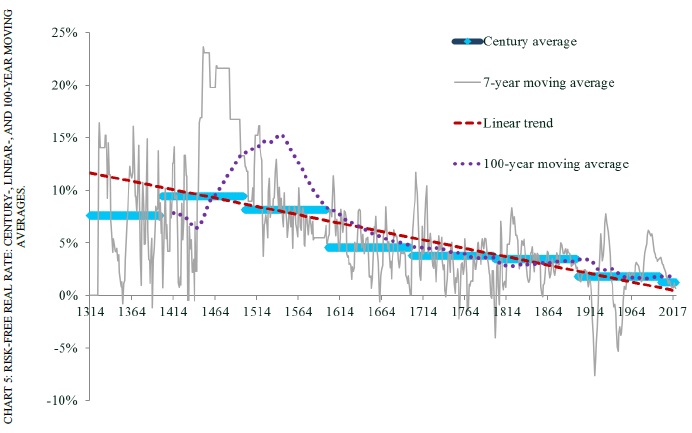

Regression and averages of real risk-free rate:

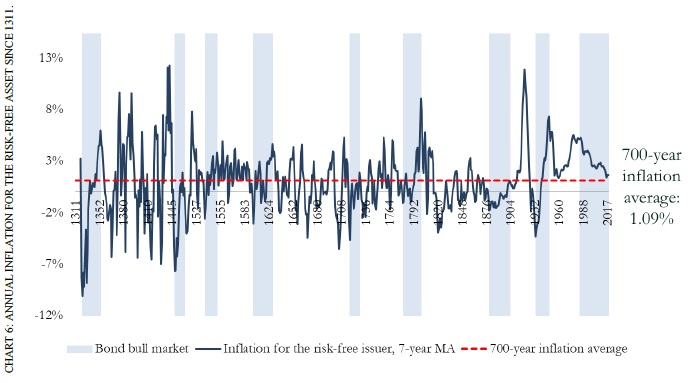

Inflation:

"

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube