A new financial research paper related to volatility selling strategies:

Autores: Sepp

Título: Gaining the Alpha Advantage in Volatility Trading

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3032098

Abstracto:

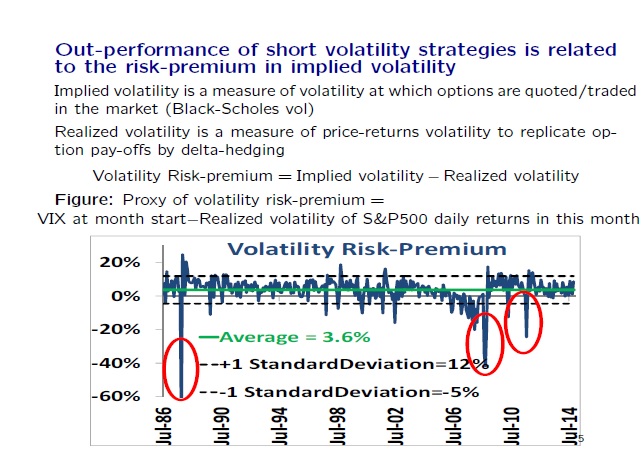

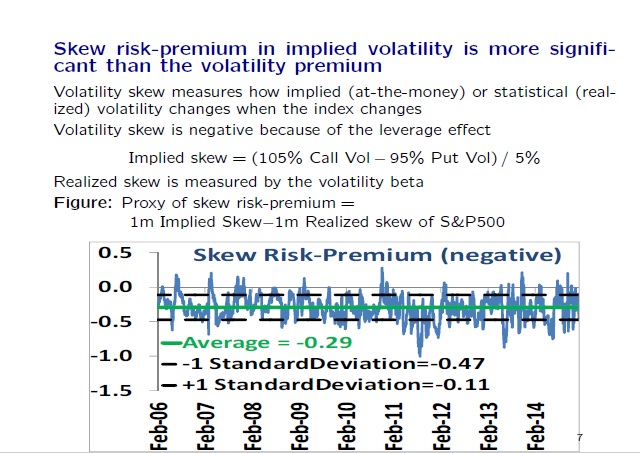

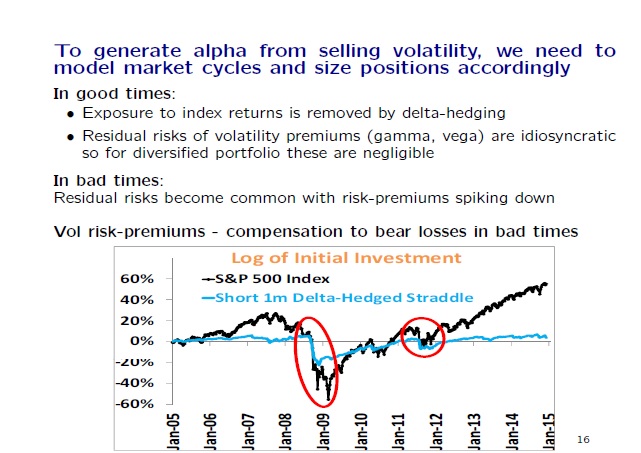

We present some empirical evidence for short volatility strategies and for the cyclical pattern of their P&L. The cyclical pattern of the short volatility strategies produces an alpha in good times but collapses to the beta in bad times. We introduce a factor model with risk-aversion to explain the risk-premium of short volatility strategies as a compensation to bear losses in bad market regimes. We then consider an econometric model for statistical inference of market regimes and for optimal position sizing. Finally, we illustrate model applications for generating alpha from volatility strategies.

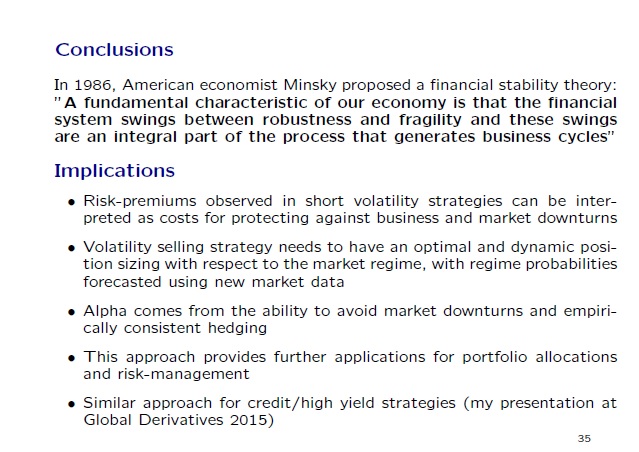

Notable presentation slides from the academic research paper:

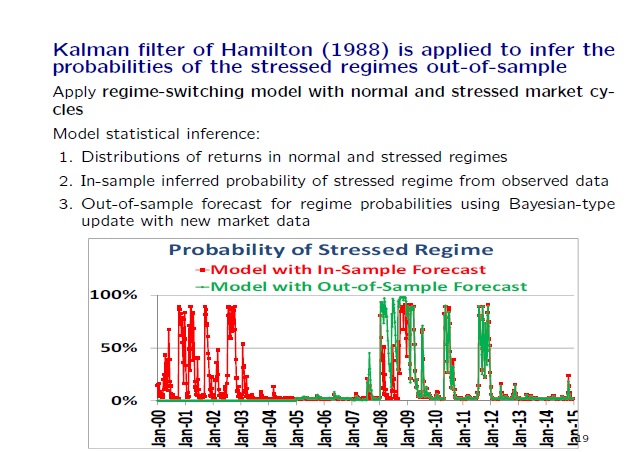

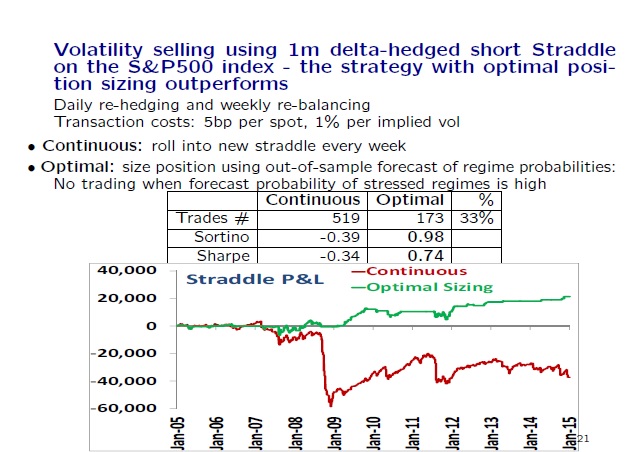

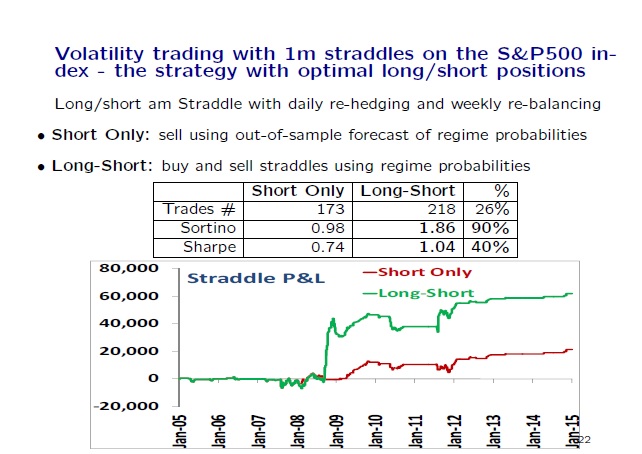

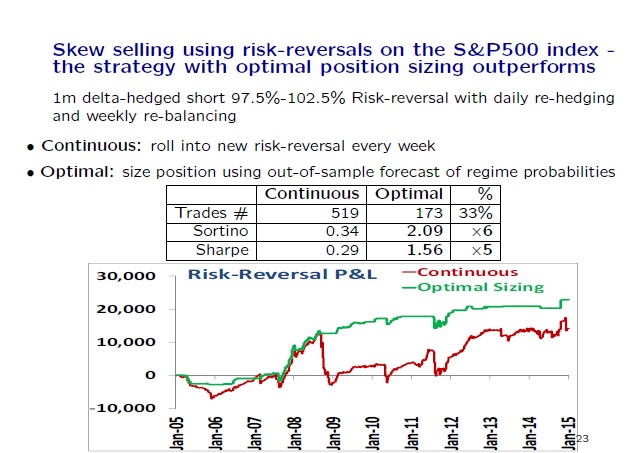

"

"

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube