An interesting paper, an analysis of a day of the week effect in the crypto currency market … :

Autores: Caporale, Plastun

Título: The Day of the Week Effect in the Crypto Currency Market

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3082117

Abstracto:

This paper examines the day of the week effect in the crypto currency market using a variety of statistical techniques (average analysis, Student's t-test, ANOVA, the Kruskal-Wallis test, and regression analysis with dummy variables) as well as a trading simulation approach. Most crypto currencies (LiteCoin, Ripple, Dash) are found not to exhibit this anomaly. The only exception is BitCoin, for which returns on Mondays are significantly higher than those on the other days of the week. In this case the trading simulation analysis shows that there exist exploitable profit opportunities that can be interpreted as evidence against efficiency of the crypto currency market.

Fragmentos destacados del artículo de investigación académica:

"There exists a vast literature analysing calendar anomalies (the Day of the Week Effect , theTurn of the Month Effect, the Month of the Year Effect, the January Effect, the HolidayEffect, the Halloween Effect etc.), and whether or not these can be seen as evidence againstthe Efficient Market Hypothesis. However, with one exception (Kurihara and Fukushima, 2017) to date no study has analysed such issues in the context of the crypto currency market – this being a newly developed market, it might still be relatively inefficient and it might offer more opportunities for making abnormal profits by adopting trading strategies exploiting calendar anomalies. We focus in particular on the day of the week effect, and for robustness purposes apply a variety of statistical methods (average analysis, Student's ttest, ANOVA, the Kruskal-Wallis test, and regression analysis with dummy variables) as well as a trading robot approach that replicates the actions of traders to examine whether or not such an anomaly gives rise to exploitable profit opportunities.

We examine daily data for 4 crypto currencies, choosing those with the highest market capitalisation and the longest data span (2013-2017), namely BitCoin, LiteCoin, Ripple and Dash. The data source is CoinMarketCap (https://coinmarketcap.com/coins/).

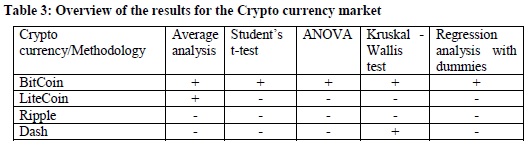

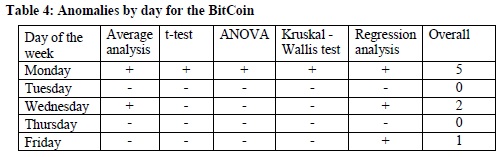

The complete set of results can be found in Appendix B. The results of the parametric and non-parametric tests are reported in Appendices C, D, E and F) and summarised in Table 3 and 4. There is clear evidence of an anomaly only in the case of BitCoin.

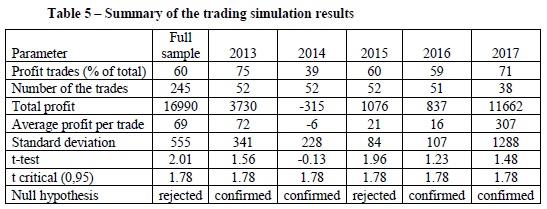

Since the anomaly occurs on Mondays (when returns are much higher than on the other days of the week) the trading strategy will be the following: open long positions on Monday and close them at the end of this day. The trading simulation results are reported in Table 5. In general this strategy is profitable, both for the full sample and for individual years, but in most cases the results are not statistically different from the random trading case, and therefore they do not represent evidence of market inefficiency.

"

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube