Hello all,

Over the last month, our team has been working on significant expansion of the “Strategy Grading” report to enhance the analysis of the chosen model portfolio (or individual strategy) compared to its peers. This improvement allows Quantpedia Pro clients to better assess the risk and performance of their selected strategy or model portfolio relative to a relevant group of strategies and ETFs, providing valuable insights into the effectiveness of their chosen approach. By enabling these comparisons, you can make more informed decisions about potential adjustments or improvements to your investment strategies.

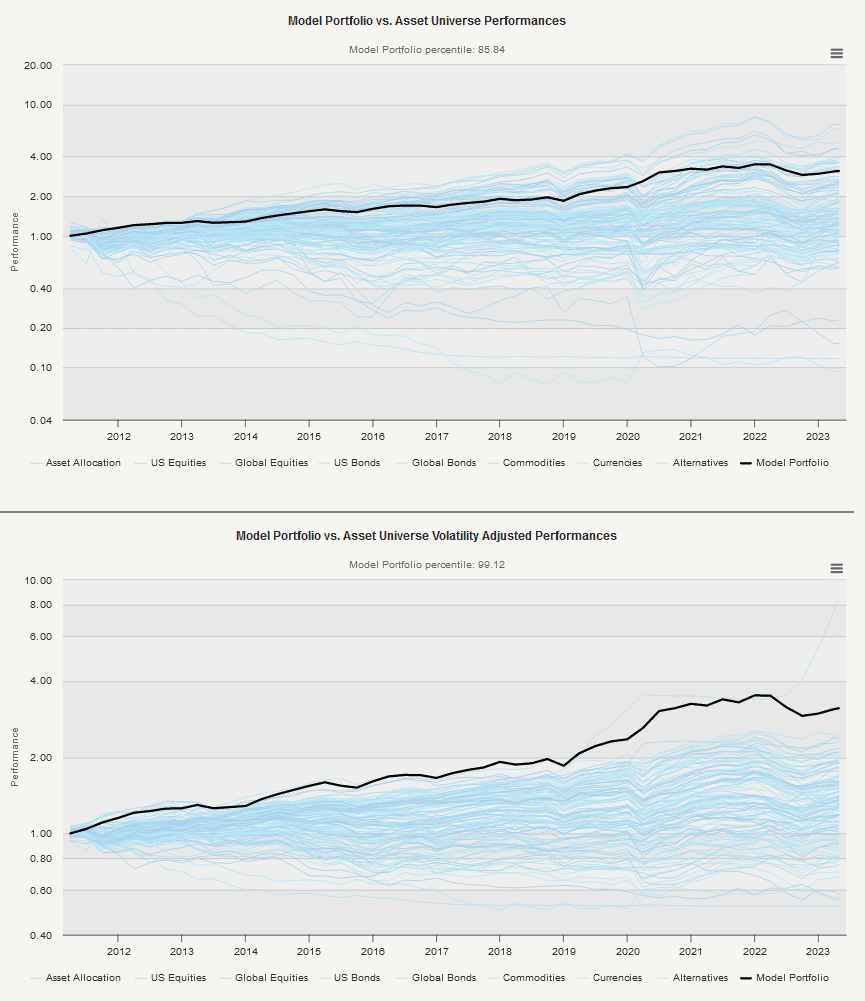

The Model Portfolio vs. Asset Universe (Volatility Adjusted) Performances charts – depict the equity curve of your selected Model Portfolio against its peers (ETFs or Quantpedia’s systematic trading strategies). The chart that shows volatility-adjusted performance rescales competing strategies to the same volatility as the selected Model Portfolio; therefore, it better shows how your portfolio fares against alternatives on a risk-adjusted basis. Of course, the higher the equity curve of your portfolio is, the better.

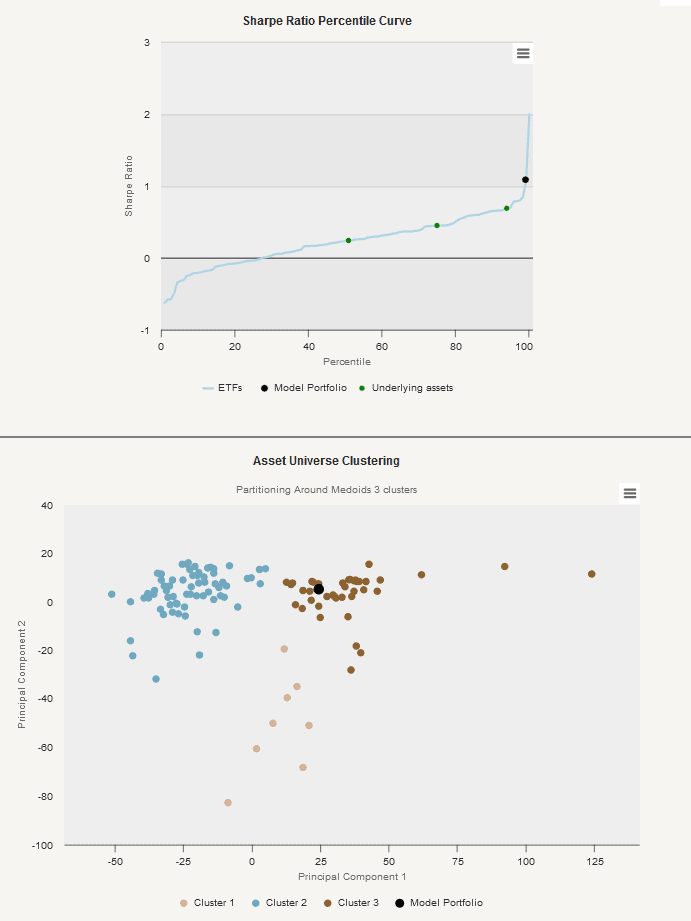

The Sharpe Ratio Percentile Curve chart displays in another way how your Model Portfolio (and its constituents) fares against ETFs or Quantpedia’s systematic trading strategies.

The Asset Universe Clustering uses the Partitioning Around Medoids clustering method to find the clusters in the universe of ETFs (or Quantpedia’s systematic trading strategies) and shows how related is the Model Portfolio to its alternatives.

Let’s also quickly recapitulate Quantpedia Premium development:

- 10 new Quantpedia Premium strategies have been added to our database

- 12 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently contains over 670 strategies with out-of-sample backtests/codes.

Additionally, 5 new articles were published on the Quantpedia blog in the previous month, 4x analysis of academic research paper and 1x Quantpedia study:

And here are links to 4x analysis of research papers:

Are Funds Flows Influenced by Mortality?

Authors: Alok Kumar, Ville Rantala, Claudio Rizzi

Title: Mortality, Mutual Fund Flows, and Asset Prices

Political Beliefs Matter for Fund Managers

Autores: Will Cassidy and Blair Vorsatz

Título: Partisanship and Portfolio Choice: Evidence from Mutual Funds

Evaluating Factor Models in China

Autores: Zhiyong Li and Xiao Rao

Título: Evaluating Asset Pricing Models: A Revised Factor Model for China

Price Momentum or Factor Momentum: What Leads What?

Autores: Nusret Cakici, Christian Fieberg, Daniel Metko, Adam Zaremba

Título: Factor Momentum Versus Stock Price Momentum: A Revisit

Yours …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube