Hello all,

As we hinted at in the blog post published a few days ago, we have a new Quantpedia Pro report ready for you – the Rebalancing Analysis. How can it help you? Our goal is to give you the possibility to quickly analyze different rebalancing frequencies and assess whats the dispersion in the performance among different rebalancing variants and determine which one is the most suitable for your portfolio.

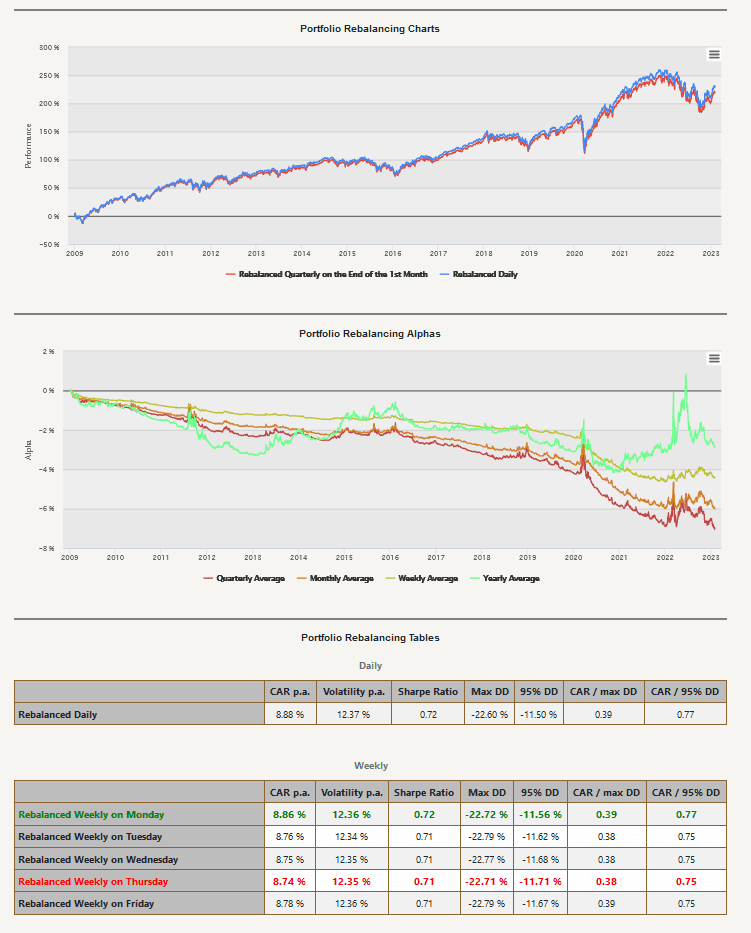

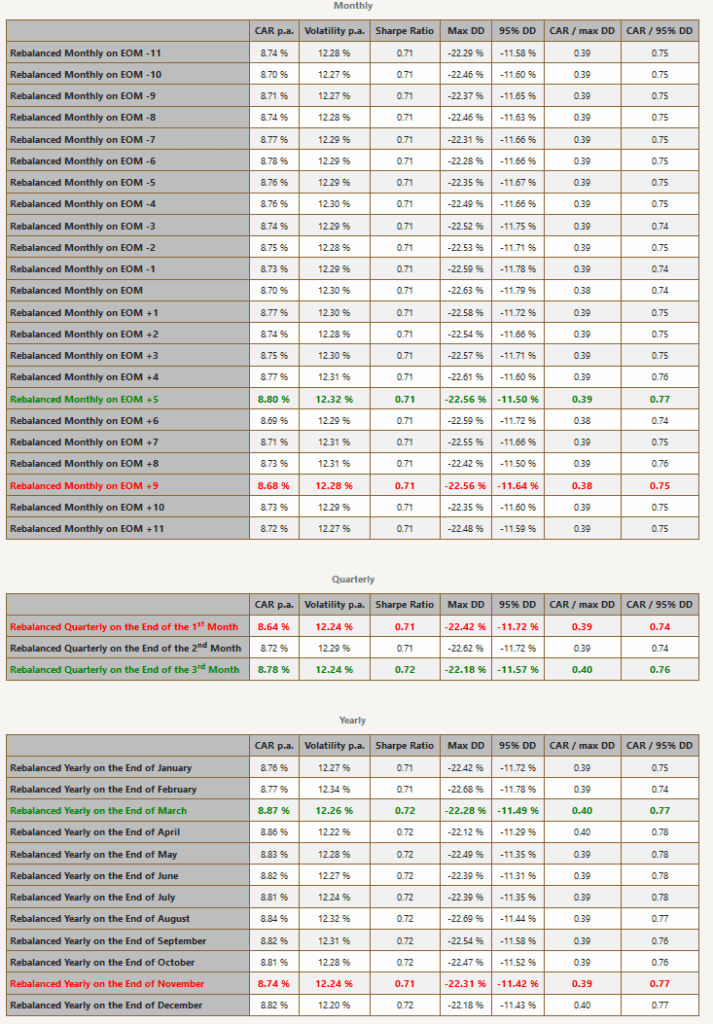

We consider daily, weekly, monthly, quarterly, and yearly rebalancing, altogether 43 versions, and show you the chart with the best and worst performing. The most important chart, the rebalancing alpha, follows. The chart shows what’s the outperformance or underperformance of the average weekly, monthly, quarterly, or yearly rebalance compared to the daily rebalanced model portfolio. The chart helps to answer the question of whether it is, on average, better to rebalance the portfolio more often or with a lesser frequency. Afterward, we present summary tables with the return and risk characteristics for each rebalancing variant, together with the performance dispersion table.

Let’s also quickly recapitulate Quantpedia Premium development:

- 9 new Quantpedia Premium strategies have been added to our database

- 10 new related research papers have been included in existing Premium strategies during the last month

- 9 new backtests were written in QuantConnect code. Our database currently contains over 630 strategies with out-of-sample backtests/codes.

Additionally, 6 new articles were published on the Quantpedia blog in the previous month, 5x analysis of academic research paper and 1x Quantpedia study:

And here are links to 5x analysis of research papers:

How to Use ETF Flows to Predict Subsequent Daily ETF Performance

Autores: Liao Xu, Xiangkang Yin and Jing Zhao

Título: Are the Flows of Exchange-Traded Funds Informative?

Which ESG Funds Perform Greenwashing?

Authors: Andrikogiannopoulou, Angie and Krueger, Philipp and Mitali, Shema Frédéric, and Papakonstantinou, Filippos

Title: Discretionary Information in ESG Investing: A Text Analysis of Mutual Fund Prospectuses

What Is an Optimal Allocation to Cryptocurrencies?

Autores: Ran Duchin, David H. Solomon, Jun Tu, Xi Wang

Título: The Cryptocurrency Participation Puzzle

Size Factor vs. Monetary Policy Regime

Autores: Marc William Simpson and Axel Grossmann

Título: The Resurrected Size Effect Still Sleeps in the (Monetary) Winter

160 Years of Wars and Disasters in Markets

Autores: Dat Mai and Kuntara Pukthuanthong

Título: Time Series and Cross-sectional Evidence from the Stock and Bond Markets

Yours …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube