Hello all,

The volatility in financial markets is still elevated, and the macro environment is challenging. Therefore, we continue to build risk management reports for our Quantpedia Pro clients. The latest addition is the Monte Carlo Analysis report, for which we unveiled our methodology approximately a week ago.

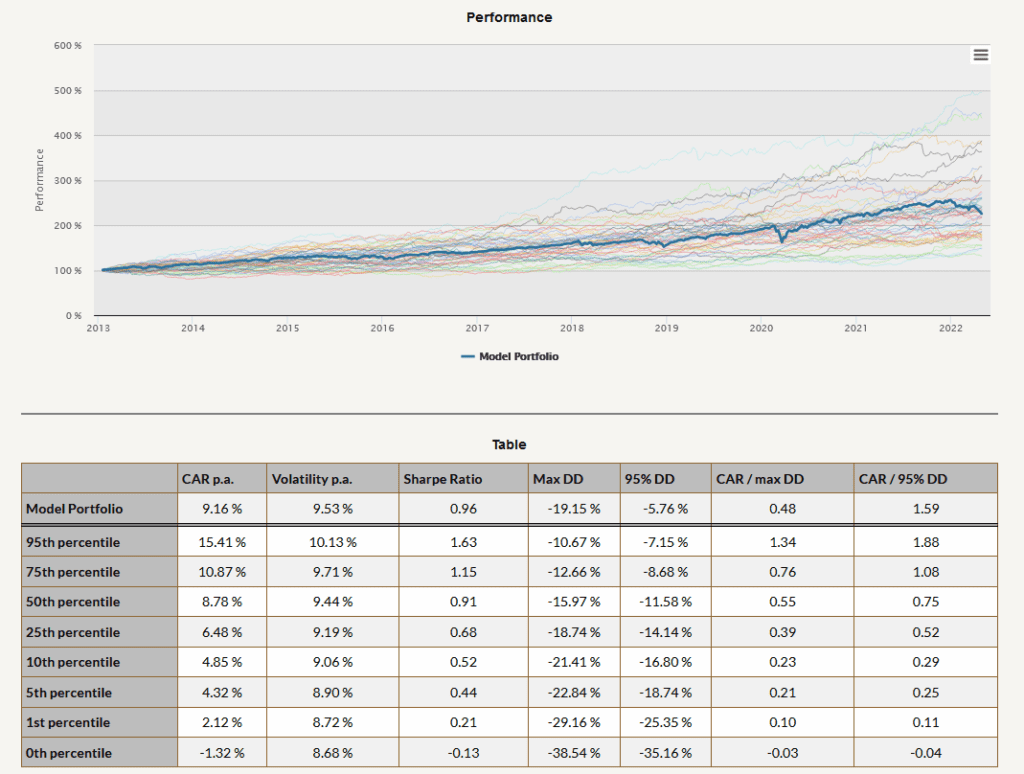

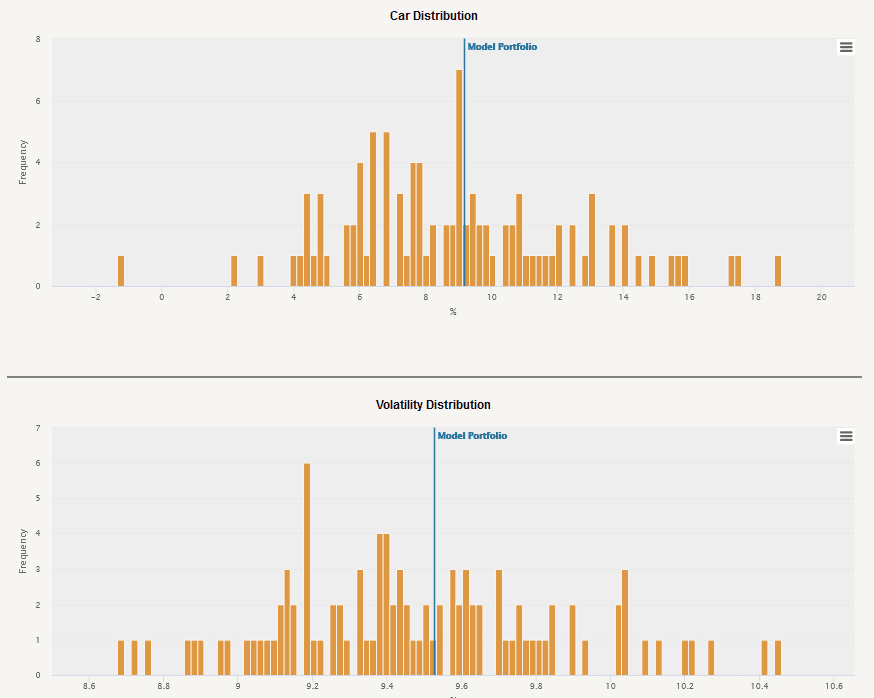

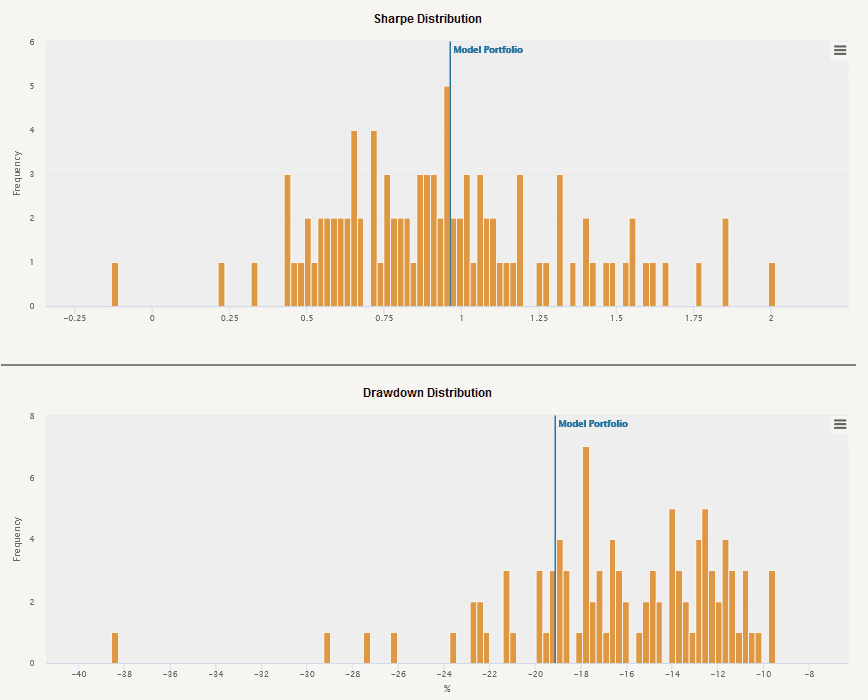

Our report uses Monte Carlo sampling with replacement. We create 100 new alternative histories of your trading strategy (or any model portfolio built in the Portfolio Manager) and review the cumulative returns of the simulated strategies and the 95th, 75th, 50th, 25th, 10th, 5th, 1st, and the 0th percentile of the risk and return characteristics. We suggest paying attention and analyzing the worst-case scenarios (10th, 5th, 1st, and the 0th percentile).

Let’s also quickly recapitulate Quantpedia Premium development:

- 9 new Quantpedia Premium strategies have been added to our database

- 15 new related research papers have been included in existing Premium strategies during the last month

- 10 new backtests were written in QuantConnect code. Our database currently contains nearly 570 strategies with out-of-sample backtests/codes.

Additionally, 8 new articles were published on the Quantpedia blog in the previous month, 3x analysis of academic research papers and 5x Quantpedia studies:

- Extending Historical Daily Bond Data to 100 Years

- Best Performing Value Strategies – Part 1

- Extending Historical Daily Commodities Data to 100 Years

- 100-Years of Multi-Asset Trend-Following

- Introduction and Examples of Monte Carlo Strategy Simulation

Analysis of research papers:

Carbon Futures – Emerging Asset with Hedging Benefits

Authors: Sercan Demiralay, Gaye Hatice Gencer, Selcuk Bayraci

Title: Carbon Credit Futures as an Emerging Asset Hedging, Diversification and Downside Risks

How Often Should We Rebalance Equity Factor Portfolios?

Authors: Emlyn Flint, Rademeyer Vermaak

Title: Factor Information Decay: A Global Study

Grading and Merging ESG Scores from Multiple Providers

Author: Invest Verte

Title: Invest Verte Framework

Yours …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube