Hello and welcome to our September recap!

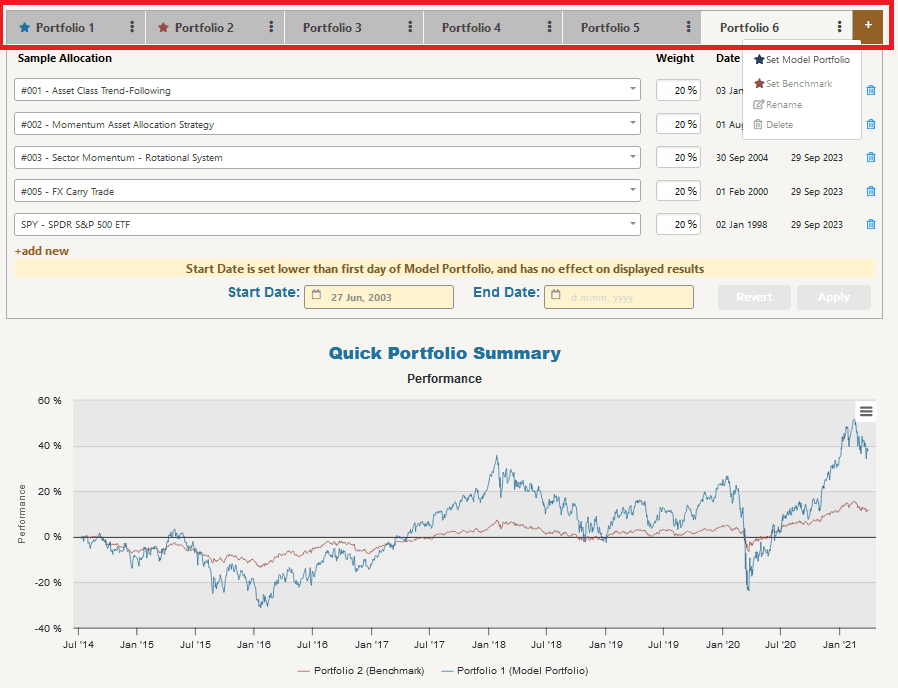

We are pleased to announce a significant technical upgrade to our Portfolio Manager, a pivotal tool for our Quantpedia Pro clients. In response to our clients’ feedback and demands, this upgrade introduces a notable enhancement to the platform’s capabilities. Following this update, clients can now create and store multiple distinct portfolios, offering unparalleled flexibility in portfolio management. Prior to this enhancement, clients were limited to maintaining only two portfolios, one for model portfolio and another for benchmark. However, with the new upgrade, our clients can now create and manage as many portfolios as required, with effortless capabilities for modification, saving, and loading of both model portfolios and benchmarks.

We believe this enhancement will provide our clients with invaluable versatility in their portfolio analysis, reaffirming our dedication to continuously improving our client’s experience.

Let’s also quickly recapitulate Quantpedia Premium development:

- 12 new Quantpedia Premium strategies have been added to our database

- 12 new related research papers have been included in existing Premium strategies during the last month

- 8 new backtests were written in QuantConnect code. Our database currently now contains nearly 710 strategies with out-of-sample backtests/codes.

Additionally, 6 new articles were published on the Quantpedia blog in the previous month:

The Seasonality of Bitcoin

Authors: Juliana Javorska, Radovan Vojtko

Title: The Seasonality of Bitcoin

Language Analysis of Federal Open Market Committee Minutes

Autores: Agam Shah and Suvan Paturi and Sudheer Chava

Título: Trillion Dollar Words: A New Financial Dataset, Task & Market Analysis

Analysis of Price-Based Quantitative Strategies for Country Valuation

Autores: Cyril Dujava, Radovan Vojtko

Título: Analysis of Price-Based Quantitative Strategies for Country Valuation

Are Commodities a Good Investment? It Depends on the Country

Autores: Vianney Dequiedt, Mathieu Gomes, Kuntara Pukthuanthong, Benjamin Williams

Título: Commodity Dependence and Optimal Asset Allocation

An Introduction to Machine Learning Research Related to Quantitative Trading

Autores: Ivana Dragonova

Título: An Introduction to Machine Learning Research Related to Quantitative Trading

Time-Varying Equity Premia with a High-VIX Threshold

Autores: Naresh Bansal and Chris T. Stivers

Título: Time-varying Equity Premia with a High-VIX Threshold and Sentiment

Plus, we have some quick info for those that were unable to attend our online conference/webinar called “A systematic approach to ESG investing“, which we co-organized with StarQube. The recording of the complete event is now available on YouTube at the following link:

Yours …

Radovan Vojtko

CEO & Head of Research

¿Buscas más estrategias para leer? Suscríbete a nuestro boletín informativo o visite nuestra Blog o Evaluador.

¿Quieres saber más sobre el servicio Quantpedia Premium? Consulta Cómo funciona Quantpedia, nuestra misión y Oferta de precios premium.

¿Quieres saber más sobre el servicio Quantpedia Pro? Compruébalo descripción, mirar videos, revisar capacidades de generación de informes y visite nuestro oferta de precios.

¿Buscas datos históricos o plataformas de backtesting? Consulta nuestra lista de Descuentos en Algo Trading.

¿Te gustaría tener acceso gratuito a? nuestros servicios? Entonces, Abre una cuenta con Lightspeed. y disfrute de un año de Quantpedia Premium sin costo alguno.

O síguenos en:

Facebook Grupo, Facebook Página, Gorjeo, LinkedIn, Medio o YouTube